Real, Unbiased Primerica Review from an Ex-MLMer

18 Comments

Table of Contents

- The United States of Primerica

- Primerica Company Overview

- How Primerica Started

- What Primerica Does

- My Primerica Experience

- Pros: Are Primerica Products Good?

- Cons: Why Primerica is Bad

- Compensation Plan: Can Primerica Make You Money?

- Primerica: Quick Summary

- Bottom Line: Will Primerica Leave You Primed For Profit?

- Shameless Plug: Realistic Passive Income Without MLM?

The United States of Primerica

Fact:

MLM companies like Primerica and Amway have been around for so long now, they’ve become a normal part of US culture.

But long before there were MLM distributors, there was another kind of annoying salesperson:

The Insurance Agent.

To be fair:

They’re obviously not all like Needlenose Ned and I actually like my personal insurance guy.

But if I get the chance to show a Bill Murray clip, you better believe that I’m gonna take it.

Every. Damn. Time.

That said, it turns out there’s a company that has managed to combine relentless insurance sales with aggressive MLM sales:

Enter Primerica.

For over 40 years now, Primerica has been selling insurance and other financial products through a network marketing business model.

And they’re doing it very well.

Primerica’s annual revenue was a cool $1.9 billion in 2018 and close to $2.1 billion in 2019.

That’s some serious scratch.

In addition to insurance, Primerica also offers investments, debt consolidation, and financial advisors who’ll say: “I highly suggest that you buy more of our sh*t”.

Kidding.

Still, the track record of Primerica is undeniable and suffice to say this MLM juggernaut knows what they’re doing.

They’ve successfully branded themselves as a “Main Street” company trying to help families build a secure financial future.

And they’ve taken their own advice to heart — building a secure financial future for the company to the tune of $9.1 billion in term life insurance.

For years, Primerica was also part of the same company known as Travelers and Citigroup.

But while you might be familiar with Travelers Insurance, you probably don’t know jack about Primerica.

Well, it’s your lucky day cuz that’s where I come in:

You’re welcome, ‘Murica.

Primerica Company Overview

Primerica’s head office is located at 1 Primerica Parkway in Duluth.

Not Minnesota but Duluth, Georgia — where it gets so hot that locals have a saying: “Duluth, Duluth, Duluth is on fire!”

Seriously.

But Duluth is also home to Primerica which mostly sells “term life” insurance and originated the slogan, “Buy Term and Invest the Difference.”

The idea is that you buy cheaper term life instead of the pricier permanent coverage, and then use what you’ve saved to invest in Primerica’s other offerings.

Simply put, term life insurance is temporary and only lasts for a set number of years that you choose up front e.g. 10, 20, or 30 years.

Term life policies only give insurance against the loss of life during the chosen term, and once it has expired, you can either renew or end the policy.

On the other hand, permanent or “whole life” insurance provides lifetime coverage against the loss of life, but also includes a cash-value savings component that can accumulate interest.

The catch is that whole life insurance costs a helluva lot more than term life and offers a very small rate of return.

Dave Ramsey does a pretty good job explaining this concept if you want more info:

Besides promoting term life, Primerica also bill themselves as “a Main Street Company for Main Street North America,” whose goal is to create more financially independent families.

In other words, while many investment companies focus solely on obtaining wealthy clients with lots of money to invest, Primerica is all about helping the middle class.

They are, after all, a network marketing company and understandably want to appeal to as many potential recruits as possible.

But for now:

Let’s rewind the clock and see how it all started over 40 years ago…

How Primerica Started

A long time ago in a galaxy far, far away….

Primerica was founded in 1977 by Arthur (“Art”) L. Williams Jr.

The same year the first Star Wars movie came out.

![]()

And just like Darth Vader, I should warn you that Primerica’s history is a little bit…

Complicated.

After his father passed away of a sudden heart attack in 1965, Art Williams learned for the first time that his family was left underinsured.

This was mostly due to his father having a whole life insurance policy that wasn’t worth much.

Art was then introduced to the concept of term life insurance, which was a lot cheaper than whole life but wasn’t well known at the time.

Believing that people were getting ripped off by expensive whole life policies that left them underinsured, Art began selling term life in 1970.

A man on a mission, he experienced immediate success but eventually grew tired of working for insurance companies who had traditional and limiting corporate structures.

In February 1977, A.L. Williams & Associates was born and the company was based on a simple philosophy:

![]()

Buy Term and Invest the Difference.

The basic idea was to show middle-America that buying term life insurance was not only better and much less expensive than whole life…

But also how they could invest what they saved into mutual funds, annuities, etc. to build long-term passive income.

The company also placed an emphasis on giving financial incentives to its sales force, and ultimately decided on the MLM business model.

Under Art’s guidance, the gamble paid off and the following decades saw A.L. Williams & Associates undergo an extensive series of acquisitions and mergers.

Don’t worry, I’ll just go over the highlights so bear with me for a minute.

- In 1980, A.L. Williams joined up with the Massachusetts Indemnity and Life Insurance Company, otherwise known as MILCO.

- MILCO was a subsidiary of PennCorp Financial, and Penncorp in turn became a subsidiary of the American Can Company in 1983.

- Four years later would change their name to Primerica Corporation.

Clear as mud? Cuz we’re just gettin’ started!

- Primerica kept acquiring more subsidiaries until they themselves were acquired in 1988 by Commercial Credit, who kept the Primerica name.

- In 1989, Primerica went public on the New York Stock Exchange (NYSE) and officially changed its name to “Primerica Financial Services”, later shortened to PFS Investments Inc.

- Four years later, Primerica acquired Travelers Insurance which became known as the Travelers Group – which finally merged with Citicorp in 1998 to create Citigroup.

A dozen years later in 2010, Citigroup decided to sell off Primerica through an initial public offering (IPO) and by 2011, Citi had completed its separation.

Today, Primerica is still publicly traded on the NYSE (PRI) and is mostly owned by large financial companies such as Fidelity and Vanguard.

PHEW!

Well that was simple, huh?

Now that my head’s about to explode, let’s explore what products Primerica actually offers.

What Primerica Does

Primerica’s bread and butter is their Term Life Insurance.

First the good news:

If you die within the term you bought the life insurance for, your policy will definitely pay out so your family will receive the money they deserve.

And Primerica has a stellar reputation for paying more than 90% of its insurance claims within just 2 weeks.

Plus, as I mentioned earlier, term life insurance is a lot cheaper than whole coverage.

So Primerica’s flagship product actually does exactly what it’s supposed to, which already puts it above many MLM companies whose products are questionable at best.

However, there are a few downsides.

First off, while their term life insurance does cost less than whole coverage, it’s still more expensive than buying term life insurance from most other companies.

The above quotes from ValuePenguin.com, show them being 11-29% more expensive than the average term life company.

Secondly, Primerica is notoriously bad at insuring anyone who happens to be in a high-risk bracket.

Basically, if you have pre-existing conditions and ain’t exactly in the peak of good health, you may find it difficult to get Primerica to sell you insurance.

And this is especially problematic because their term insurance policies offer no conversion options to whole life insurance.

See, most other insurance companies – hell, pretty much every reputable term life insurance company – allow the policy holder to convert their term insurance to a permanent policy without needing to underwrite it again.

Many folks start by buying term insurance, then might have a change in life circumstance and decide they want the reliable coverage of permanent insurance.

And as long as your company isn’t Primerica, you don’t need to reapply — you can just convert your term insurance to permanent coverage and you’re all set.

But Primerica doesn’t allow for conversions to permanent coverage, which means that you’ll just have to apply for term insurance again.

And once again, if you’re no longer in great health, Primerica may not cover you at all.

(Or if they do take you, expect to pay a LOT more.)

In short, Primerica life insurance seems to be a good product for healthy peeps, but it may be pricier than you can get elsewhere.

If you Google their website (www.primerica.com), the company also offers:

- Car and home insurance

- Long-term care insurance

- Personal Finance vehicles such as mutual funds, managed investments, annuities, and business retirement plans.

![]()

Primerica also partners with Pre-Paid Legal (aka LegalShield) to offer things like legal protection and ID theft protection.

Legalshield is an MLM company with its own list of issues that I may address one day in its own post, but suffice to say their “legal protection” is reportedly sub-standard.

Finally, Primerica’s DebtWatchers program involves a partnership with Equifax, giving customers access to credit monitoring, budget tracking, and tips to help pay down your debt.

While these services might be useful, you might wanna check out other places who offer comparable services for FREE (instead of charging your credit card $15/mo).

That’ll save you almost $200 per year, which might be more helpful to a person in debt.

Just sayin’.

My Primerica Experience

Back when I was about 15 years old, I was on summer break when my father signed up to be a Primerica rep.

It was my very first introduction to network marketing and I vividly remember “John” — the local RVP — driving up in his 7-series BMW and wearing a massive gold ring.

He was super-friendly and sat down with my old man at our kitchen table, as I secretly listened in on their conversation from the other room.

They talked about how much my father hated his sales job, what his financial needs and wants were, and how Primerica was the fastest way to build something called “total financial independence”.

Even though I was just a kid, it all sounded amazing and I was immediately hooked.

Apparently, so was my father who signed up that night and officially began his Primerica journey.

I remember him studying for his insurance exams and making calls to our neighbors to “take a look at something” they might be interested in.

Although he didn’t like “mixing business with pleasure” as he called it, my father was persistent and kept at it until he started to see some success.

I even recall my father going to a national event in Atlanta with his team, while I stayed home in Canada and devoured all the Primerica material he had.

My personal favorites were the sales training tapes from a guy named Tom Hopkins and a book written by A.L. Williams himself called All You Can Do Is All You Can Do But All You Can Do Is Enough!

Just the other day, I was looking through some boxes and found an old Primerica training manual called “Principles For Success”.

Even though it was published in 1993, the information is still just as excellent and relevant today on how to get your mind right and become an effective leader.

To this day, I still believe that you’d be hard-pressed to find better mindset training than in a reputable MLM company like Primerica.

But I digress.

After school started in the fall, I quickly lost interest in my father’s new business venture and I think he did as well.

Slowly but surely he stopped going to meetings until one day when I asked how Primerica was going, he simply told me it wasn’t for him anymore.

And that was that.

But I never forgot that first introduction to multi-level marketing, and still can’t believe that 20 years later I’m actually writing a blog about it lol.

Life’s a trip.

Pros: Are Primerica Products Good?

✓ Main product (term life insurance) actually delivers.

This is a nice change from many MLMs who are hawking fountain-of-youth creams or magic body wraps like It Works!

But Primerica’s products all generally do what they’re supposed to.

Their term insurance covers your butt and pays out if you die, and their mutual funds are real investments which could make you money long-term.

✓ High market appeal.

Most folks would like to protect their family in case they die prematurely.

They also wanna save money.

This is why “Buy Term and Invest the Difference” is such a great slogan and has lasted for over 40 years.

After all, who doesn’t want their family to be taken care of, if something bad happens to them?

It’s also not a bad idea to have a long-term investment strategy in place.

✓ Been around a long time.

If you’re an MLM company and have lasted for over four decades, congratulations — you’re in rarified network marketing air.

Primerica has been operating since the late 1970s and is a pretty rock-solid company overall.

Can’t forget that they were once part of the same group as Travelers Insurance and Citibank.

And this reputation is clearly worth something because Primerica was named one of Forbes 50 most trustworthy companies in 2015.

✓ A little charity goes a long way.

Like most MLMs, Primerica has a charitable arm: The Primerica Foundation which offers grants to charities like family services organizations.

They also encourage their own employees to donate to charity.

In fact, the combined might of their employees raised half a million dollars for the American Cancer Society in 2017 and 2018.

Respect.

Cons: Why Primerica is Bad

✗ It’s an MLM.

Despite having legit financial products, at the end of the day Primerica is still a network marketing company.

Which means to be truly successful, you’ll need to recruit a large team below you.

Not my cuppa tea but whatever works for you boss.

✗ High-priced insurance.

In order to build in enough profit for the company along with you and your upline, Primerica’s products typically cost more than comparable financial products elsewhere.

This is one of the big reasons that Primerica does not offer any online quotes.

Customers can only get Primerica’s prices by talking to an agent like you, and it’s your job to convince them to buy immediately without shopping around.

This may be easier said than done because…

✗ No conversion options and no high-risk individuals need apply.

While Primerica does offer term insurance that will pay out if you die during the specified term, the fact that it can’t be converted to whole coverage is a bummer if you change your mind.

They also won’t accept high-risk individuals meaning your physical condition better be tip-top if you’d like to be insured by them.

✗ Legal issues.

In 2014, Primerica had to set aside $15.4 Million to settle 238 lawsuits from Florida public servants.

Apparently, the government doesn’t like it when you steer a bunch of firefighters, teachers, and other public workers into low-quality, high-risk investments for the personal gain of the sales team.

Go figure.

But this hasn’t stopped Primerica from continuing to flourish, taking on well over 100,000 new sales recruits annually, and earning annual revenues of two billion dollars.

✗ License to Bill.

By law, Primerica’s sales reps are not allowed to sell insurance and securities without a license.

This means that in order to sell Primerica’s products, you’ll need to pass an actual licensing exam.

As a bonus, this will take at least 90 days, during which you’ll have to pay to be a Primerica member but can’t actually sell all their flagship products.

Time to hit the books!

Compensation Plan: Can Primerica Make You Money?

Given that Primerica won’t give online quotes for how much their insurance costs, it’s not surprising to learn that they don’t post their compensation plan online either.

Which is really annoying.

But don’t worry, I found the numbers for ya anyway.

So bite me Primerica 🙂

Now, the most important number in any MLM is how much commission you make as an entry-level representative, since most MLM members never make it beyond entry level.

And for Primerica, your entry level commission is… well, nothing at first.

See, the trick about Primerica is that until you are licensed, you can’t actually sell their main insurance or investment products.

The video below isn’t the greatest, but it’s the best I could find to explain their basic comp plan:

According to that video, you’re technically allowed to sell some of Primerica’s lesser products while waiting to get licensed (can’t confirm this) but the bottom line is, you need to get licensed before you can make any real money.

Now let’s talk turkey.

- It’ll cost you around $100 just to sign up for Primerica in the first place.

- If you want access to their members-only website, Primerica Online — that’s another $25 per month.

- According to the company, Primerica Online is “an entire suite of tools specifically created to help you succeed at building a lasting and rewarding business” which includes support resources, the best training webinars, your own Primerica email address, and a personalized website.

But keep in mind that it normally takes at least 3 months to get your required licenses.

So just be aware that you’ll start somewhere between negative $100 and negative $175 as you learn about Primerica and prepare for your exams.

If and when you pass your licensing exams, you are now an official Primerica Representative and entitled to basic commission levels.

For insurance plans, this is 25% of the first premium for a 25-year plan. So if the premium is $1000 per year, you will earn $250 upfront.

That’s actually a pretty nice payout for making one sale.

However, it’s worth noting that if a customer defaults on their premium payments within their first year, Primerica will hit you with a chargeback for that money.

In other words, you won’t really know if you get to keep all your commission money for another 12 months.

That said, most folks that want to have life insurance are doing it for their family’s protection, so unless you’re signing up those who really don’t want or need it, your defaults should (hopefully) be low.

- For investments, the Representative commission is 30% of the dealer cut, which is usually a small number like 4.5%. So if someone invests $1000, you’ll make around $13.

- For loans, the Representative commission is 0.312%. So if you manage to sign someone up for a $10,000 debt consolidation loan, you’ll make $31.

Those numbers are a lot smaller, but at least they don’t come with the potential for chargebacks.

Still, it does show very clearly that — just like in any MLM — the only way to make any real money is to recruit more salespeople (build your downline).

Once you directly recruit 3 new associates (“3 Directs”), you qualify as a Senior Representative.

While this slightly bumps up your personal commissions (e.g. 35% instead of 25% on insurance sales), the real bonus here is now you can receive bonuses from your new recruits below you.

The first way you make money from your downline is your standard overrides.

In this case, your override is 10% so if the Representative you recruited sells $1000 of premium insurance, you get $100 (subject to chargebacks).

While very few sales reps will ever see the highest levels, District Leaders (who sell $2500 of premiums in a single month and have a Senior Rep below them) get a 50% commission on their annual premiums and a 15-25% override.

Division Leaders selling double that get another 10% kick, Regional Leaders hiring multiple Division Leaders earn an additional 10%, and at the top of the food chain is the highest level:

Regional Vice Presidents who are basically treated like gods in the Primerica universe.

Primerica Insurance Commissions

*Mobile users: Scroll left/right on table if your screen can't fit all 4 columns| LEVEL | OWN SALES | OVERRIDES | REQUIREMENTS |

|---|---|---|---|

| Associate | - | - | Sign up with Primerica |

| Representative | 25% | - | Get your life insurance license |

| Senior Representative | 35% | 10% | Recruit 3 new Associates, complete your FNA |

| District Leader | 50% | 15-25% | Promote 1 new SR, generate $2500 in premiums |

| Division Leader | 60% | 10-35% | Promote 1 new DL, generate $5000 in premiums |

| Regional Leader | 70% | 10-45% | Promote 2 new DLs, generate $7500 in premiums |

| Regional Vice President | 95% | 10-70% | Promote 6+ DLs, $20,000 in premiums, get securities license |

Besides getting overrides, Primerica has a second way you can make money from your downline which is unique and a lil shady in my arrogant opinion.

See, for those first 90 days, your newly recruited associates can’t legally sell anything.

But they’re still paying Primerica and are supposed to be learning about the business.

And the way Primerica tells them to do that is by watching the expert who hired them.

That means YOU.

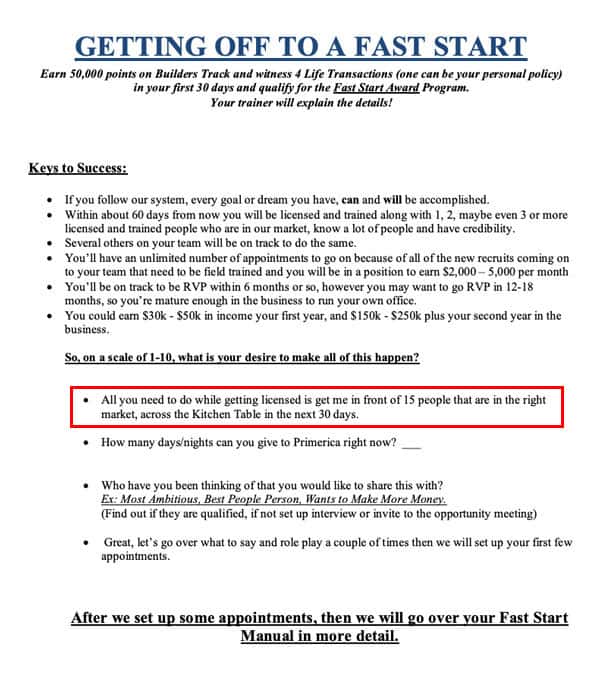

In other words, your new recruits are encouraged to make a list of their prospective friends/family members and invite you to sell insurance to them while they “watch and learn”.

I actually found an unofficial “Fast Start Manual” from a Primerica rep that shows what I mean below:

Long story short: you get to make money from selling to your recruit’s best leads.

Sounds good in theory, but don’t forget that it works both ways – your upline will also get the chance to sell to YOUR best leads while you’re in training.

So it’s kinda like being an apprentice – you gotta pay your dues and earn your way up the ladder.

And of course, the higher you go, the better the money gets.

According to a Primerica-affiliated website I found:

When representatives earn $50,000 in a 12-month period, they’re awarded a special watch. When they reach $100,000 in income, they’re rewarded with a special ring that signifies membership into the exclusive Financial Independence Council. New diamonds are added to the ring with every additional $100,000 they earn.

Long story short, success breeds success.

And big frickin’ rings.

Primerica: Quick Summary

| PROS | CONS |

|---|---|

| Primerica's main product (term life insurance) is something most people need and actually delivers. | Primerica is still a network marketing company which means you'll need to recruit in order to make any real money. |

| Not only do they provide protection for you and your family, but Primerica also offers long-term investment strategies. | Primerica's insurance typically costs more than comparable financial products, does not have conversion options, and only applies to low-risk individuals. |

| They've been around for over 40 years and are a rock-solid company overall. | Like most MLMs, they have ongoing legal issues and lawsuits. |

| Primerica and its employees donate a significant amount to charity. | In order to sell Primerica's main products, you'll need to study for and pass an actual licensing exam. |

Bottom Line: Will Primerica Leave You Primed For Profit?

Here’s the deal:

Primerica may not offer any convenient compensation charts online, but they are legally obligated to offer a little information in the form of this disclosure statement.

And there’s a lot more information in their annual report.

Clockin’ in at 188 pages, it obviously wasn’t meant to be read by humans.

But consider me a helpful explanation robot, beep boop.

Here’s some interesting numbers from page 8 of the annual report:

In 2017, there were 303,867 new recruits, but only 48,535 newly licensed sales reps.

That means only 16% of Primerica recruits ended up passing the licensing exam in 2017.

In other words, 84% of folks who joined Primerica not only failed to make any money, they never even qualified to make any money.

That’s… pretty bad.

But then again, it actually makes sense.

Passing an insurance exam probably ain’t easy.

I’m gonna guess it wasn’t as simple as getting my GED (good enough diploma) after dropping outta high school.

In any case, you can’t sell any Primerica insurance without passing the exam.

Here are some more numbers for ya:

Primerica had a total of 126,121 licensed reps in 2017 and 116,827 in 2016.

That means they added roughly 9,300 licensed reps overall.

But wait a minute, didn’t we just say that they added 48,535 newly licensed reps above?

My math skills are absolute dogsh*t but I think that means nearly 40,000 licensed reps quit in a year.

That’s almost a third of the entire licensed sales force!

Here’s the thing:

The reality of network marketing is that to make any REAL money, you gotta be constantly building your downline.

Cuz if 1 out of 3 licensed reps quit every year…

And you need to have 3 reps in your downline to earn any override commissions…

Well, I think you get the point.

(Isn’t math fun?)

Still:

Some think Primerica is just another pyramid scheme or scam.

Others manage to make this business opportunity work.

They believe that becoming full-time or part-time Primerica agent is the best decision they ever made.

But if you average in all the top million-dollar earners in 2017, Primerica paid out an average of $6,030 to their licensed sales reps.

That’s about $500 per month.

Think about this for a moment:

If you’re one of those rare individuals who’s good with numbers and has no problem taking a licensing exam, why not just go get a job selling insurance?

Actual insurance sales jobs pay, on average, a helluva lot more than $6k per year.

Like, 8 times as much.

On the other hand, if you’re looking for ways to make money online that don’t require selling insurance or recruiting your friends and family…

Shameless Plug: Realistic Passive Income Without MLM?

Imagine this:

No recruiting, no selling products, no rah-rah meetings, no bullsh*t.

Don’t believe me?

Don’t blame you.

But before you scream “SCAM!” and scram, do yourself a favor.

Put down the Hatorade and click here to discover more realistic ways to make passive income from home.

While its quite accurate that Primerica has an MLM based structure… in this particular case I don’t think it’s a bad thing.

I’m pretty resistant to MLM based businesses, but I’ve been looking into Primerica for a couple of reasons –

First off, it’s a reasonably simple way to get things like your life and mutual funds licences.

A couple of things you missed – there is actually a “training bonus” that new recruits are entitled to, and it’s actually fairly generous.

It’s not mentioned in the Fast Start document you presented, but it is income that new recruits can earn while working on their licence, and observing.

And you mentioned the commission rates for investments but there is a bit more to it than what you present – the commission are monthly – so as you build your book, you build your income.

Thanks for your comment, Chris. Appreciate your input 🙂

While I agree that joining Primerica is a way to get licensed, less than 20% actually pass the licensing exam (according to Primerica’s annual report).

And while it’s possible to build a huge book of residual commissions, the average Primerica rep makes around $500 per month. Facts.

But I wish you the best of luck man 👍

There’s a Primerica team nearby that is trying to recruit me. I am licensed from a prior employer so it’s even better for them.

This team seems genuinely interested in educating folks first and foremost. Obviously after the education, there’s the offer of Primerica products.

I like the idea of helping folks and I don’t necessarily need to make a whole lot of money since I’d be doing it a little here and there.

The issues is, I’ve read reviews that rank their insurance towards the bottom in the industry. There’s numerous complaints about slow payouts and issues with getting paperwork submitted. I don’t want to have my name attached to lousy insurance.

Ultimately, I like the concept of educating Americans on how to be more fiscally responsible. I just wish their products were better. The MLM part isn’t attractive either.

Thanks for your comment, Chuck! I appreciate your insight 🙂

Thanks for your post. It’s really helped me to understand because my MVP never showed me how the business works.

I started a month ago in this MLM, I never heard about this company before but my intention is learn about this business and obviously earn money.

I’m doing the test for the life insurance policy and it sucks. My native language is Spanish and it’s difficult to do it.

In this company, the people who really win are the ones who are on top and have good teams.

My question is: How many people do I have to recruit to earn a minimum $1,000 monthly?

Thanks!

Thanks for your comment, Angie 🙂

I agree with you — in any MLM, the one’s who build the biggest teams generally make the most money.

But you should really ask your upline for a better explanation of the compensation plan and how to start building your downline.

Good luck!

Excellent article! I’m over 60 so have seen many MLM’s come and go over the years. They always fail over time, because most people don’t want to push products on friends and family.

Most of us want to buy a product off a shelf (or website), without someone pushing us to do so.

We’ll accept advice from friends who have knowledge and aren’t getting a commission off what we buy.

When I hear about bonuses and fancy gifts for employees, I know who is paying for that: the customer — paying more than they need to, to finance many layers of profit-takers.

Thanks for your comment, Ben!

I like you man 🙂 You are straight up and no bullsh*ting around. Thanks for the review and my name is Simon also.

Great names think alike, thanks man 🙂

Bro, you are hilarious! I am a financial advisor and was looking into working for Primerica. Thank you for opening my eyes. I did my due diligence and got my answer.

Thanks Ed, appreciate the feedback!

Hey Simon, great article.. There are companies out there that will subsidize the training, prioritize client needs and benefits, and you do not need to ‘recruit’ to be successful. We seem to have become a society that likes the sizzle of fast money. For guy that gota GED you know your stuff. thanks

Thanks Richerd 🙂

Wow thanks so much for this perspective, some recruiters just don’t paint the picture that way! Of course only doing what they know best, sell!

Glad you liked it, Alize!

Hi Simon!

Thank you for this awesome information it really helps!

First time I have fun while reading a review 🙂

Glad to hear it Bernice, thanks for your comment!